How to Estimate Start Up Capital for Starting a Business

- Small Business

- Types of Businesses to Start

- Start Up Businesses

- ')" data-event="social share" data-info="Pinterest" aria-label="Share on Pinterest">

- ')" data-event="social share" data-info="Reddit" aria-label="Share on Reddit">

- ')" data-event="social share" data-info="Flipboard" aria-label="Share on Flipboard">

How to Start a Portable Concrete Pump Company

How to write a restaurant proposal, why is it important for entrepreneurs to develop financial plans for their companies.

- How to Do a Successful Product Launch

- Examples of Project Cost Assumptions

Startup capital includes funds for any expenses to be incurred before launching a company, and capital required after launch to run the company until it reaches positive cash flow -- when revenues are higher than expenses.

Accurately estimating the capital required to start a company is critical because running out of capital can cause the company to fail in its very early stages. With careful estimates based on sound assumptions, the chances of a cash shortfall are reduced.

Create a Detailed Business Plan

Creating a business plan with forecasts is essential to figuring out how much you'll need to launch and run your business, advises the U.S. Small Business Administration. Describe the products and services you will be offering, and the strategies you intend to deploy to introduce them to the market.

Determine when each strategy will be implemented, such as the schedule for advertising and what media you intend to use. Include a budget that includes your costs to launch the business and run it for the first year. Including revenue projections will help you estimate how much money you will need to get your business off the ground and operate it during year one.

Calculate Product Development Costs

Consult with your vendors or suppliers, and obtain estimates of what these costs will be. Work out precise estimates rather than wide ranges.

Prepare a marketing budget. The strategic marketing plan provides you with information about what your marketing tactics will be. Now attach numbers to these tasks based on consultation with vendors you have selected and researching what other companies in your industry typically spend.

Put together a personnel budget. Forecast the number of employees and management team members you will need for the first three years. Break this out by department so you make sure you don't overlook any functional areas.

Forecast facilities and equipment cost. Determine how much space your venture needs to conduct operations. This can be office space, retail space, and production and warehouse space depending on the type of company. Ask real estate professionals for information about the rate per square foot for the type of space you will need. Remember to include office equipment leases in your equipment forecast, for items such as computer workstations and telephone systems.

Forecast general and administrative expenses. These costs include items such as office supplies, travel, insurance, legal and accounting fees.

Separate Launch and Operating Expenses

Separate out the costs that will be incurred before launching the company from those that will be incurred on an ongoing basis after the company is launched, recommends small-business website BPlans .

Complete a revenue forecast. Build financial models with assumptions about unit sales volume and price, and then generate a spreadsheet with forecast revenues, month by month for the first three years. Total up the expenses you forecast for each of these months, and calculate how long it will take for the company to reach breakeven cash flow. Total the cash deficit for these months.

Compute your total startup capital. Add up capital needed prior to launch and the capital required to fund the cash deficit. This is your total startup capital. It is extremely difficult to accurately forecast how quickly revenues will grow in a start up venture. Take this into account by adding 10 percent to 20 percent to the capital you think you need. Low-ball your projected income estimates to give you a cushion, as well.

- BPlans: Estimating Realistic Startup Costs

- Schedule each new person you hire to come on board when they are absolutely needed, not before, so you can save on personnel costs.

- Plan on securing a short-term lease for the minimum square footage you need to get started, with an option to acquire more space if the company grows as fast as you forecast.

- It is extremely difficult to accurately forecast how quickly revenues will grow in a start up venture. Take this into account by adding 10 percent to 20 percent to the capital you think you need.

Related Articles

Developing a financial plan for a small business, what is a revenue budget, how to calculate a budgeted profit, how to write a 3-year business forecast, what is an annualized budget, objectives of a feasibility study, how to open a pumpkin farm, main steps in business planning, how to prepare and manage a budget, most popular.

- 1 Developing a Financial Plan For a Small Business

- 2 What Is a Revenue Budget?

- 3 How to Calculate a Budgeted Profit

- 4 How to Write a 3-Year Business Forecast

Planning, Startups, Stories

Tim berry on business planning, starting and growing your business, and having a life in the meantime., business plan financials: starting costs.

It’s really important to have an idea of what you need before you start. Continuing with my series on standard business plan financials , startups need to project starting costs. Starting costs set up a starting balance, which is necessary to plan cash flow. And the starting costs are critical to determining whether a startup can bootstrap or needs outside funding. For existing companies that already have financial results, projections start with the expected ending balance of the previous period. But for startups, it’s about starting costs.

Starting costs are essentially the sum of two kinds of spending. You can estimate them both in two simple lists:

- Startup expenses : These are expenses that happen before the beginning of the plan, before the first month of operations. For example, many new companies incur expenses for legal work, logo design, brochures, site selection and improvements, and signage. If there is a business location, then normally the startup pays rent for a month or more before opening. And if employees start receiving compensation before the opening, then those disbursements are also startup expenses.

- Startup assets : Typical startup assets are cash (the money in the bank when the company starts), business or plant equipment, office furniture, vehicles, and starting inventory for stores or manufacturers.

A Simple Starting Costs Example

I’ve used a bicycle store as an example in several posts that are part of this series of standard business plan financials. Here’s a visual in spreadsheet form, of sample starting costs for a hypothetical bicycle store.

Notice that the lists for estimating starting costs, on the left in the illustration above, are matched to another list of starting funding, on the right side of the illustration. Books have to balance, so the initial estimates need to include not just the money you spend, but also where it comes from. In the case above, Garrett had to find $124,500, and you can see that he financed it with Accounts Payable, debt, and investment in various categories.

Another Simple Starting Costs Example

Here is another simple example: the starting costs worksheet that Magda developed for the restaurant I used for a sample sales forecast . Magda’s list includes rent and payroll, the same as in her monthly spending, but here they are included in starting costs because these expenses happen before the launch.

I included rent and payroll because they point out the importance in timing. The difference between these as startup expenses and running expenses is timing, and nothing else. Magda could have chosen to plan startup expenses as a running worksheet on expenses, starting a few months before launch, as in the illustration below. The launch in this case is early January, so the expenses for October through December are startup expenses. I prefer the separate lists, because I like the way the two lists create an estimate of starting costs. But that’s an option.

The LivePlan Alternative

If you’re a LivePlan user, the LivePlan interface assumes this method and has a more intuitive interface than the spreadsheet version I’m showing in this post. For LivePlan, you start your plan when you start spending, regardless of launch date. So the spending you do for rent and salaries and such, before launch, is part of the flow, as above. Also, LivePlan has its own guided way of helping you figure out what assets you need, how much they cost, and how you are going to finance starting costs, to set up your balance. And the LivePlan cash flow estimator will help you decide how much cash you need, so you don’t have to follow the spreadsheet method here (below).

How to Estimate Your Starting Costs

Obviously the goal with starting costs isn’t just to track them, but to estimate them ahead of time so you have a better idea, before you start a new business, of what the financial costs might be. Breaking the items down into a practical list makes the educated guess a lot easier. Ideally, you know the business you want to start, you are already familiar with the industry, so you can do a useful estimate for most of the startup costs from your own experience. If you don’t have enough firsthand knowledge, then you should be talking to people who do. For others, such as insurance, legal costs, or graphic design for logos, call some providers or brokers, and talk to partners; educate those guesses.

Starting Cash is the Hardest and Most Important

How much cash do you need in the bank, as you launch? That’s usually the toughest starting cost question. It’s also prone to misinformation, such as those alleged rules of thumb you can find everywhere, saying you need to have a year’s worth of expenses, or six months’ worth, before you start. It’s not that simple. For most businesses, the startup cash isn’t a matter of what’s ideal, or what some expert says is the rule of thumb – it’s how much money you have, can get, and are willing to risk.

The best way is to do a Projected Cash Flow while leaving the supposed starting cash balance at zero, which shows how much (at least in theory, according to assumptions) the startup really needs in cash to support the business as it grows, before it reaches a monthly cash flow break-even point. Magda did that to determine the $12,000 needed as starting cash for her restaurant. Note how, in the illustration here, the lowest point in cash is slightly less than $12,000:

That low point comes, theoretically, in the third month of the business, March. The low point is $11,609. Obviously that’s just an educated guess, but it’s based on assumptions for sales forecast, expense budget, and important cash flow factors including sales on account and purchasing inventory. So it’s better than a stab in the dark, or some rule of thumb. Just as an example, the total spending with the estimates shown here, the theoretical “year’s worth of spending,” is $182,000 (which you don’t see on the illustration, by the way, but take my word for it). The total for the first six months is $93,000. If Magda sticks to those old formulas, she can’t start the business. She is able to raise enough money, between loans and her savings, to put $12,000 into the starting cash balance. So that’s what she does. Then she launches and continues to have her monthly reviews, and watch the performance of all key indicators very carefully.

Leave a Reply Cancel reply

Your email address will not be published. Required fields are marked *

Save my name, email, and website in this browser for the next time I comment.

The quickest way to turn a business idea into a business plan

Fill-in-the-blanks and automatic financials make it easy.

No thanks, I prefer writing 40-page documents.

Discover the world’s #1 plan building software

- school Campus Bookshelves

- menu_book Bookshelves

- perm_media Learning Objects

- login Login

- how_to_reg Request Instructor Account

- hub Instructor Commons

- Download Page (PDF)

- Download Full Book (PDF)

- Periodic Table

- Physics Constants

- Scientific Calculator

- Reference & Cite

- Tools expand_more

- Readability

selected template will load here

This action is not available.

1.4: Chapter 4 – Initial Business Plan Draft

- Last updated

- Save as PDF

- Page ID 21278

- Lee A. Swanson

- University of Saskatchewan

Learning Objectives

After completing this chapter, you will be able to

- Develop a comprehensive business plan draft

This chapter describes an approach to writing your draft business plan. It also outlines the elements of a comprehensive business plan that can be used as a template for starting your business plan.

Figure 7 – Initial Business Plan Draft (Illustration by Lee A. Swanson)

Effective Business Plans

Effective business plans

- Provide statements that are backed by evidence or data

- Include context and references with every table, figure, or illustration

- Include relevant, clear, concise tables and financial information, and exclude unnecessary material

- Present timelines for distinct purposes

- Use clear sections customized to the particular business or its environment rather than generic sections

Writing the Draft Business Plan

Although there are various ways to approach the task of writing a draft business plan, one effective approach is to do the following:

- This will provide you with a template for the information needed for your plan.

- You can copy and paste the results of your essential initial research into the sections of your business plan template where you believe that they can be used to support or justify the strategies and other decisions you will later describe in those sections. Of course, you can later move those parts of your environmental scan as needed as you develop your plan. In general, this strategy results in a stronger business plan .

- Completing this step will give you the satisfaction of seeing some of your work so far taking shape in the form of a business plan.

- Also, inserting the results from your environmental scan into the relevant sections of your plan should later provide you with the stimulus and support you will need to develop solid, realistic, evidence-based strategies and decisions for those sections.

- Incorporate your business model into your new business plan template. As there is no section in a business plan in which you specifically describe your business model, you will need to incorporate your business model elements into appropriate sections of your plan.

- You will normally include both information that you got from particular sources and information based on an assumption you made (and that you might intend to replace later with more accurate information from valid sources).

Follow these practices as you develop your plan:

- When you do this, you help establish your credibility as a business plan writer, and your business plan’s credibility. It also might save you time later when you discover that you need to add a similar item along with its cost to your list.

- Note: Do not reinvent the wheel by “inventing” your own method to reference your sources and do not use multiple methods. Use one (and only one) proper and well-established referencing method, like APA. This will improve the degree of professionalism of your plan.

- Note: if you are an expert source on something—maybe you are a construction expert that business plan readers will trust to do estimates on building costs—you should establish your credentials and clearly indicate when some of the information in your plan is based on your own expert knowledge.

- When you flag your assumptions in this way, you can quickly and easily see what information needs to be replaced with sourced information before you finalize your business plan.

- Projecting realistic sales can be difficult, but setting up a method for doing so early gives business plan writers a significant start toward completing their business plan. A well-developed sales model that takes advantage of the powers of electronic spreadsheets gives business plan writers the opportunity to relatively quickly and easily make necessary changes to their assumptions and overall estimates when needed.

- When you use the schedules provided on the spreadsheet templates, and any others that you add, you will be well on your way to developing the financial component of your business plan.

General Business Plan Format

Letter of transmittal.

A letter of transmittal is similar to the cover letter of a resume. The letter of transmittal should be tailored to the reader, clearly identifying the customized ask of the potential investor or lender. It should be short and succinct, delineating the ask (i.e. funding, specialized recruiting, purchasing a product or service, obtaining advice, etc.) within a few paragraphs. It should not summarize the business plan, as that is the job of the executive summary.

- Includes nice, catchy, professional, appropriate graphics to make it appealing for targeted readers

Executive Summary

- Can be longer than normal executive summaries—up to three pages

- Written after remainder of plan is complete

- Includes information relevant to targeted readers as this is the place where they are most likely to form their first impressions of the business idea and decide whether they wish to read the rest of the plan

Table of Contents

List of tables.

- References every table, figure, and appendix within the text of the plan so the relevance of each of these elements is clear.

List of Figures

Introduction.

- Indicates the purpose for the plan

- Appeals to targeted readers

Business Idea

- May include description of history behind the idea and the evolution of the business concept if relevant

Value Proposition

- Explains how your business idea solves a problem for your expected customers or otherwise should make them want to purchase your product or service instead of a competitor’s

- Outlines what you intend for the venture to be

- Inspires all members of the organization

- Helps stakeholders aspire to achieve greater things through the venture because of the general direction provided through the vision statement

After articulating a good vision, the business plan writer should consider what achieving the vision looks like. Many business plan writers write their vision and leave it at that. The problem with this approach is that they often then do not take the necessary steps to illustrate how the strategies they outline in their plan will move them toward achieving their vision. If they make this mistake, their strategies might indicate that they are fulfilling their current mission, but are not taking steps to move beyond that.

Vision statements should be clear with context throughout the business plan. For example, if the goal is to be the premier business operating in that industry in Saskatchewan, does that mean you have one location and are considered the best at what you do it even though you only have a small corner of the market, or does it mean that you have many locations across the province and enjoy a large market share?

- Should be very brief—a few sentences or a short paragraph

- Indicates what your organization does and why it exists—may describe the business strategy and philosophy

- Consists of five to ten short statements indicating the important values that will guide everything the business will do

- Outlines the personal commitments members of the organization must make, and what they should consider to be important

- Defines how people behave and interact with each other

- Should be reflected in all of the decisions outlined in the business plan, from hiring to promotions to location choices

- Helps the reader understand the type of culture and operating environment this business intends to develop

Major Goals

- Describes the major organizational goals

- Specific, Measurable, Action oriented, Realistic, and Timely [SMART]

- Realistic, Understandable, Measureable, Believable, and Achievable [RUMBA]

- Aligns with everything in plan

- Written, or re-written as the second last thing you do before finalizing your business plan by proofreading, polishing, and printing it (writing the Executive Summary is the final thing you should write)

Operating Environment

Trend analysis.

- However, consider whether this is the right place for this analysis: it may be better positioned, for example, in the Financial Plan section to provide context to the analysis of the critical success factors, or in the Marketing Plan to help the reader understand the basis for the sales projections.

Industry Analysis

- Includes an analysis of the industry in which this business will operate

- As above, consider whether this is the right place for this analysis: it may be better placed, for example, in the Marketing Plan to enhance the competitor analysis, or in the Financial plan to provide context to the industry standard ratios in the Investment Analysis section.

Of course, your trend analysis will also include a market-level analysis (using a set of questions, like those listed in Chapter 2) and a firm-level analysis (using tools like a SWOT Analysis / TOWS Matrix, various forms of financial analyses, a founder fit analysis, and so on), but those analyses are usually best placed in other sections of your plan to support the strategies and decisions you present there. The market-level analysis will inevitably fit in the Marketing Plan section, but the firm-level analysis might be spread across some or all of the Operating Plan, Human Resources Plan, Marketing Plan, and Financial Plan sections.

Operations Plan

- Given these constraints, what is your operating capacity (in terms of production, sales, etc.)?

- What is the work flow plan for your operation?

- What work will your company do and what work will you outsource?

Operations Timeline

- When will you make the preparations, such as registering the business name and purchasing equipment, to start the venture?

- When will you begin operations and make your first sales?

- When will other milestone events occur such as moving operations to a larger facility, offering a new product line, hiring new key employees, and beginning to sell products internationally?

- Sometimes it is useful to include a graphical timeline showing when these milestone events have occurred and are expected to occur.

Business Structure and other Set-up Elements

- Sole Proprietorship

- Partnership

- Limited Partnership

- Corporation

- Cooperative

Note: Your financial statements, risk management strategy, and other elements of your plan are affected by the type of legal structure you choose for your business. For example, all partnerships should have a clear agreement outlining the duties, expectations, and compensation of all partners as well as the process of dissolution. Spreadsheet templates are formatted for corporations and will need to be formatted for other forms of businesses.

- Zoning, equipment prices, suppliers, etc.

- Leasing terms, leasehold improvements, signage, pay deposits, etc.

- Getting business license, permits, etc.

- Setting up banking arrangements

- Setting up legal and accounting systems (or professionals)

- Ordering equipment, locks and keys, furniture, etc.

- Recruiting employees, setting up the payroll system and benefit programs, etc.

- Training employees

- Testing the products/services that will be offered

- Testing the systems for supply, sales, delivery, and other functions

- Creating graphics, logos, promotional methods, etc.

- Ordering business cards, letter head, etc.

- Setting up supplier agreements and outlining why those sellers are preferred

- Buying inventory, insurance, etc.

- Revising business plan

- And many more things, including, when possible, attracting purchased orders in advance of start-up through personal selling (by the owner, a paid sales force, independent representatives, or by selling through brokers wholesalers, catalogue houses, retailers), a promotional campaign, or other means

Note: As part of your business set-up, you need to determine what kinds of control systems you should have in place, establish necessary relationships with suppliers prior to your start-up, and generally deal with a list of issues like those mentioned above.

- What is required to start-up your business including the purchases and activities that must occur before you make your first sale?

- When identifying capital requirements for start-up, a distinction should be made between fixed capital requirements and working capital requirements.

Fixed Capital Requirements

- What fixed assets, including equipment and machinery, must be purchased so your venture can conduct its business?

- May also show the financing required, often in the form of longer-term loans

Working Capital Requirements

- What money is needed to operate the business (separately from the money needed to purchase fixed assets) including the money needed to purchase inventory and pay initial expenses?

- May also show the financing required. Working capital is usually financed with operating loans, trade credit, credit card debt, or other forms of shorter-term loans

Risk Management Strategies

- Enterprise – liability exposure for things like when someone accuses your employees or products you sell of injuring them

- Financial – securing loans when needed and otherwise having the right amount of money when you need it

- Operational – securing needed inventories, recruiting needed employees in tight labour markets, operating when customers you counted on not purchasing product as you had anticipated, managing theft, arson, and natural disasters like fires and floods, etc.

- Avoid – choose to avoid doing something, outsource, etc.

- Reduce – through training, assuming specific operational strategies, etc.

- Transfer – insure against, outsource, etc.

- Assume – self-insure, accept, etc.

Figure 8 – Risk Management Strategies (Illustration by Lee A. Swanson)

Operating Processes

- What operating processes will you apply?

- How will you ensure your cash is managed effectively?

- How will you schedule your employees?

- How will you manage your inventories?

- If you will have a workforce, how will you manage them?

- How will you bill out your employee time?

- How will you schedule work on your contracts?

- How you will manufacture your product (process flow, job shop, etc.?)

- How will you maintain quality?

- How will you institute and manage effective financial monitoring and control systems that provide needed information in a timely manner?

- How will you manage expansion?

- May include planned layouts for facilities

- What are your facility plans?

- Expressed as a set physical location

- Expressed as a set of requirements and characteristics

- How large will your facility be and why must it be this size?

- How much will it cost to buy or lease your facility?

- What utility, parking, and other costs must you pay for this facility?

- What expansion plans must be factored into the facility requirements?

- What transportation and storage issues must be addressed by facility decisions?

- What zoning and other legal issues must you deal with?

- What will be the layout for your facility and how will this best accommodate customer and employee requirements?

Organizational Structure

- May include information on Advisory Boards or Board of Directors from which the company will seek advice or guidance or direction

- May include an organizational chart

- Can be a nice lead-in to the Human Resources Plan

Human Resources Plan

- How do you describe your desired corporate culture?

- What are the key positions within your organization?

- How many employees will you have?

- What characteristics define your desired employees?

- What is your recruitment strategy? What processes will you apply to hire the employees you require?

- What is your leadership strategy and why have you chosen this approach?

- What performance appraisal and employee development methods will you use?

- What is your organizational structure and why is this the best way for your company to be organized?

- How will you pay each employee (wage, salary, commission, etc.)? How much will you pay each employee?

- What are your payroll costs, including benefits?

- What work will be outsourced and what work will be completed in-house?

- Have you shown and described an organizational chart?

Recruitment and Retention Strategies

- Includes how many employees are required at what times

- Estimates time required to recruit needed employees

- Employment advertisements

- Contracts with employment agency or search firms

- Travel and accommodations for potential employees to come for interviews

- Travel and accommodations for interviewers

- Facility, food, lost time, and other interviewing costs

- Relocation allowances for those hired including flights, moving companies, housing allowances, spousal employment assistance, etc.

- May include a schedule showing the costs of initial recruitment that then flows into your start-up expense schedules

Leadership and Management Strategies

- Outlines your leadership philosophy

- Explains why it is the most appropriate leadership approach for this venture

- What training is required because of existing rules and regulations?

- How will you ensure your employees are as capable as required?

- Health and safety (legislation, WHMIS, first aid, defibulators, etc.)

- Initial workplace orientation

- Financial systems

- Product features

Performance Appraisals

- Identifies how you will manage your performance appraisal systems

Health and Safety

- Notes any legal requirements (and also legal requirements for other issues that may be included in other parts of the plan)

- Identifies accreditation you might pursue, such as ISO 9000, and if so, evaluates the costs, benefits, and time frame

- Outlines training for employees, such as WHMIS training or machinery handling training

Compensation

- Always justifies your planned employee compensation methods and amounts

- Always includes all components of the compensation (CPP, EI, holiday pay, etc.)

- Identifies how you will ensure both internal and external equity in your pay systems

- Describes any incentive-based pay or profit sharing systems planned

- May include a schedule that shows the financial implications of your compensation strategy and supports the cash flow and income statements shown later

Key Personnel

- May include brief biographies of the key organizational people

Marketing Plan

- You must show evidence of having done proper research, both primary and secondary. If you make a statement of fact, you must back it up with properly referenced supporting evidence. If you indicate a claim is based on your own assumptions, you must back this up with a description as to how you came to the conclusion.

- It is a given that you must provide some assessment of the economic situation as it relates to your business. For example, you might conclude that the current economic crisis will reduce the potential to export your product and it may make it more difficult to acquire credit with which to operate your business. Of course, conclusions such as these should be matched with your assessment as to how your business will make the necessary adjustments to ensure it will thrive despite these challenges, or how it will take advantage of any opportunities your assessment uncovers.

- If you apply the Five Forces Model, do so in the way in which it was meant to be used to avoid significantly reducing its usefulness while also harming the viability of your industry analysis. This model is meant to be used to consider the entire industry, not a subcomponent of it (and it usually cannot be used to analyze a single organization).

- Your competitor analysis might fit within your assessment of the industry, or it might be best as a section within your marketing plan. Usually a fairly detailed description of your competitors is required, including an analysis of their strengths and weaknesses. In some cases, your business may have direct and indirect competitors to consider. Maintain credibility by demonstrating that you fully understand the competitive environment.

- Assessments of the economic conditions and the state of the industry appear incomplete without accompanying appraisals outlining the strategies the organization can/should employ to take advantage of these economic and industry situations. So, depending upon how you have organized your work, it is usually important to couple your appraisal of the economic and industry conditions with accompanying strategies for your venture. This shows the reader that you not only understand the operating environment, but that you have figured out how best to operate your business within that situation.

- Outlines an effective analysis of your venture (see the Organizational Analysis section below)

Market Analysis

- Usually contains customer profiles, constructed through primary and secondary research, for each market targeted

- Contains detailed information on the major product benefits you will deliver to the markets targeted

- Describes the methodology used and the relevant results from the primary market research completed

- If there was little primary research completed, justifies why it is acceptable to have done little of this kind of research and/or indicate what will be done and by when

- Includes a complete description of the secondary research conducted and the conclusions reached

- Define your target market in terms of identifiable entities sharing common characteristics. For example, it is not meaningful to indicate you are targeting Canadian universities. It is, however, useful to define your target market as Canadian university students between the ages of 18 and 25, or as information technology managers at Canadian universities, or as student leaders at Canadian universities. Your targeted customer should generally be able to make or significantly influence the buying decision.

- You must usually define your target market prior to describing your marketing mix, including your proposed product line. Sometimes the product descriptions in business plans seem to be at odds with the described target market characteristics. Ensure your defined target market aligns completely with your marketing mix (including product/service description, distribution channels, promotional methods, and pricing). For example, if the target market is defined as Canadian university students between the ages of 18 and 25, the product component of the marketing mix should clearly be something that appeals to this target market.

- Carefully choose how you will target potential customers. Should you target them based on their demographic characteristics, psychographic characteristics, or geographic location?

- You will need to access research to answer this question. Based on what you discover, you will need to figure out the optimum mix of pricing, distribution, promotions, and product decisions to best appeal to how your targeted customers make their buying decisions.

Competition

- However, this information might fit instead under the market analysis section.

- Describes all your direct competitors

- Describes all your indirect competitors

- If you include a competitor positioning map, insure that the x-axis and y-axis are meaningful. Often, competitor maps include quality and price as axes. Unless you can clearly articulate the distinction between high quality and low quality, it may be more valuable to have more meaningful axes or describe your value proposition relative to your competitors in the absence of a positioning map.

Figure 9 – Competitor Positioning Map (Illustration by Lee A. Swanson)

- You must clearly communicate the answers to these questions in your business plan in order to attract the needed support for your business. One caution is that it may sound appealing to claim you will provide a superior service to the existing competitors, but the only meaningful judge of your success in this regard will be customers. Although it is possible some of your competitors might be complacent in their current way of doing things, it is very unlikely that all your competitors provide an inferior service to that which you will be able to provide.

Marketing Strategy

- Covers all aspects of the marketing mix: your promotional decisions, product decisions, distribution decisions, and pricing decisions

- Outlines how you plan to influence your targeted customers to buy from you (your optimum marketing mix, and why is this one better than the alternatives)

Organizational Analysis

- Leads in to your marketing strategy or is positioned elsewhere depending upon how your business plan is best structured

- If doing so, ALWAYS ensure this analysis results in more than a simple list of internal strengths and weaknesses and external opportunities and threats. A SWOT analysis should always prove to the reader that there are organizational strategies in place to address each of the weaknesses and threats identified and to leverage each of the strengths and opportunities identified.

- An effective way to ensure an effective outcome to your SWOT Analysis is to apply a TOWS Matrix approach to develop strategies to take advantage of the identified strengths and opportunities while mitigating the weaknesses and threats. A TOWS Matrix evaluates each of the identified threats along with each of the weaknesses and then each of the strengths. It does the same with each of the identified opportunities. In this way strategies are developed by considering pairs of factors.

- The TOWS Matrix is a framework with which to help you organize your thoughts into strategies. Most often you would not label a section of your business plan as a TOWS Matrix because this would not add value for the reader. Instead, you should describe the resultant strategies—perhaps while indicating how they were derived from your assessment of the strengths, weaknesses, opportunities, and threats. For example, you could indicate that certain strategies were developed by considering how internal strengths could be employed toward mitigating external threats faced by the business.

Product Strategy

- If your product or service is standardized, you will need to compete on the basis of something else—like a more appealing price, having a superior location, better branding, or improved service. If you can differentiate your product or service, you might be able to compete on the basis of better quality, more features, appealing style, or something else. When describing your product, you should demonstrate that you understand this.

Pricing Strategy

- If you intend to accept payment by credit card (which is probably a necessity for most companies), you should be aware of the fee you are charged as a percentage of the value of each transaction. If you don’t account for this you risk overstating your actual revenues by perhaps one percent or more.

- Sales forecasts must be done on at least a monthly basis if you are using a projected cash flow statement. These must be accompanied by explanations designed to establish their credibility for readers of your business plan. Remember that many readers will initially assume your planned time frames are too long, your revenues are overstated, and you have underestimated your expenses. Well crafted explanations for all of these numbers will help establish credibility.

Distribution Strategy

- If you plan to use e-commerce, you should include all the costs associated with maintaining a website and accepting payments over the Internet.

Promotions Strategy

- As a new entrant into the market, must you attract your customers away from your competitors they currently buy from or will you be creating new customers for your product or service (i.e. not attracting customers away from your competitors)?

- If you are attracting customers away from competitors, how will these rivals respond to the threat you pose to them?

- If you intend to create new customers, how will you convince them to reallocate their dollars toward your product or service (and away from other things they want to purchase)?

- In what ways will you communicate with your targeted customers? When will you communicate with them? What specific messages do you plan to convey to them? How much will this promotions plan cost?

- If your entry into the market will not be a threat to direct competitors, it is likely you must convince potential customers to spend their money with you rather than on what they had previously earmarked those dollars toward. In your business plan you must demonstrate an awareness of these issues.

- Consider listing the promotional methods in rows on a spreadsheet with the columns representing weeks or months over probably about 18 months from the time of your first promotional expenditure. This can end up being a schedule that feeds the costs into your projected cash flow statement and from there into your projected income statements.

- If you phone or visit newspapers, radio stations, or television stations seeking advertising costs, you must go only after you have figured out details like on which days you would like to advertise, at what times on those days, whether you want your print advertisements in color, and what size of print advertisements you want.

- Carefully consider which promotional methods you will use. While using a medium like television may initially sound appealing, it is very expensive unless your ad runs during the non-prime times. If you think this type of medium might work for you, do a serious cost-benefit analysis to be sure.

- Some promotional plans are developed around newspaper ads, promotional pamphlets, printing business cards, and other more obvious mediums of promotion. Be certain to, include the costs of advertising in telephone directories, sponsoring a little league soccer team, producing personalized pens and other promotional client give-always, donating items to charity auctions, printing and mailing client Christmas cards, and doing the many things businesses find they do on-the-fly. Many businesses find it to be useful to join the local chamber of commerce and relevant trade organizations with which to network. Some find that setting a booth up at a trade fair helps launch their business.

- If you are concerned you might have missed some of these promotional expenses, or if you want to have a buffer in place in case you feel some of these opportunities are worthwhile when they arise, you should add some discretionary money to your promotional budget. A problem some companies get into is planning out their promotions in advance only to reallocate some of their newspaper advertisement money, for example, toward some of these other surprise purposes resulting in less newspaper advertising than had been intended.

Financial Plan

- Contains financial statements

- Various funding options and exit strategies for potential investors

- Business valuation (be cautious not to over value your business)

- Break-even analysis

Business Valuation

There are a multitude of sophisticated business valuation methodologies. A rule of thumb for business valuations is a multiple of its earnings. For example, if the chosen multiple is five and the business’ earnings before taxes are $55M, the business’ valuation would be approximately $275M.

Break-Even Analysis

Break-Even Point = FC/(P-VC)

- FC = Fixed Costs

- P = Unit Price

- VC = Variable Cost

Example: If the business’ total fixed costs are $1,000,000.00, it costs $5.00 to produce the widget, and the business sells the widget for $7.00, the break-even point is 500,000 widgets.

- You will most certainly need to make monthly cash flow projections from business inception to possibly three years out. Your projections will show the months in which the activities shown on your fixed capital and working capital schedules will occur. This is nearly the only way to clearly estimate your working capital needs and, specifically, important things like the times when you will need to draw on or can pay down your operating loans and the months when you will need to take out longer-term loans with which to purchase your fixed assets. Without a tool like this you will be severely handicapped when talking with bankers about your expected needs. They will want to know how large of a line of credit you will need and when you anticipate needing to borrow longer-term money. It is only through doing cash flow projections that you will be able to answer these questions. This information is also needed to determine things like the changes to your required loan payments and when you can take owner draws or pay dividends.

- Your projected cash flows are also used to develop your projected income statements and balance sheets.

Pro forma Cash Flow Statements

Pro forma income statements, pro forma balance sheets, investment analysis, projected financial ratios and industry standard ratios, critical success factors (sensitivity analysis), list of items a business may need to purchase.

- Business license

- Registration for name, etc.

- Domain name registration

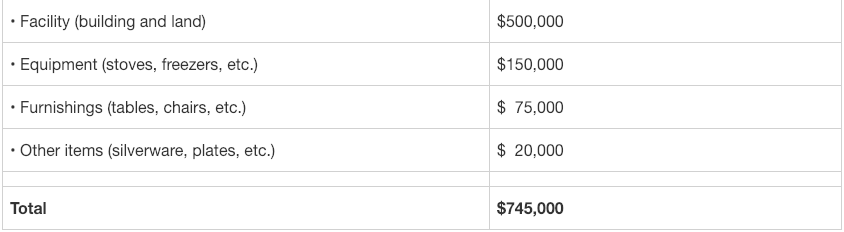

- Initial product inventory

- All the little things like curtains/blinds, decorations, microwave for staff room, etc.

- All the things needed to run the business from day #1 (like cutlery, plates, cooking pots, table settings etc. for restaurants; like towels, soap, etc. for gyms; like equipment and so on for manufacturing and service places)

- Set-up and testing of new facilities—new factories and offices do not operate at peak efficiency for some time after start-up because it takes time for the new systems to kick into high gear

- Professional services needed

- Lawyer’s fees to make sure agreements are solid

- Graphic designer or design company needed to develop visuals

- Accounting firm needed to set up initial systems

- Insurance—maybe not a direct cost to this one to account for

- Accounting system software

- Computer, printer, other things needed like scanner

- Office furniture

- Initial office supplies—paper, pens, etc.

- Internet/wifi

- Microwave and coffee maker and similar supplies for staff room or coffee room

- Bank fees—business banking is normally not free—might also need to have business cheques

Customer Interaction

- Cash register

- Loyalty cards/system

Production/Operations

- Safety equipment (fire extinguishers, AED)

- Security systems

- Equipment maintenance

- Janitorial services and cleaning supplies

- Bathroom supplies—toilet paper, soap, towels

- Membership costs for various associations, including the local chamber of commerce, any professional associations for the relevant industry, etc.

- Subscriptions for things like important trade publications, etc.

- Shelving and storage systems

- Even when not full restaurant, operations like coffee shops still require equipment like dishwasher

- Safety—prior to start-up and ongoing and for new employees

- Ads, travel expenses—flights, hotels, taxi rides, meal allowances, etc.—to recruit people through interviews, meeting meals, set up with real estate agents, etc.

- Website development

- Costs for setting up and managing social media (can take a lot of an employee’s time)

- Grand opening costs

- If buying, include property taxes and all utilities in cash flows and income statement and include building maintenance and maybe build up a reserve fund to pay for things like future roof repairs and needed renovations and upgrades

- If renting/leasing, include rental/least cost and whatever utilities are not included in rental/lease payment

Renovations

- Construction

- Utility hookups

- Inspections

- Interior signage

- Fencing, parking lot, exterior lighting, other exterior things

Risk Management

- Insurance (need to choose the types needed)

- Training costs

- Things like snow removal, de-icing sidewalks, etc.

Chapter Summary

This chapter described the basic elements of a comprehensive business plan.

- Starting a Business

- Growing a Business

- Small Business Guide

- Business News

- Science & Technology

- Money & Finance

- For Subscribers

- Write for Entrepreneur

- Entrepreneur Store

- United States

- Asia Pacific

- Middle East

- South Africa

Copyright © 2024 Entrepreneur Media, LLC All rights reserved. Entrepreneur® and its related marks are registered trademarks of Entrepreneur Media LLC

Elements of a Business Plan There are seven major sections of a business plan, and each one is a complex document. Read this selection from our business plan tutorial to fully understand these components.

Now that you understand why you need a business plan and you've spent some time doing your homework gathering the information you need to create one, it's time to roll up your sleeves and get everything down on paper. The following pages will describe in detail the seven essential sections of a business plan: what you should include, what you shouldn't include, how to work the numbers and additional resources you can turn to for help. With that in mind, jump right in.

Executive Summary

Within the overall outline of the business plan, the executive summary will follow the title page. The summary should tell the reader what you want. This is very important. All too often, what the business owner desires is buried on page eight. Clearly state what you're asking for in the summary.

The statement should be kept short and businesslike, probably no more than half a page. It could be longer, depending on how complicated the use of funds may be, but the summary of a business plan, like the summary of a loan application, is generally no longer than one page. Within that space, you'll need to provide a synopsis of your entire business plan. Key elements that should be included are:

- Business concept. Describes the business, its product and the market it will serve. It should point out just exactly what will be sold, to whom and why the business will hold a competitive advantage.

- Financial features. Highlights the important financial points of the business including sales, profits, cash flows and return on investment.

- Financial requirements. Clearly states the capital needed to start the business and to expand. It should detail how the capital will be used, and the equity, if any, that will be provided for funding. If the loan for initial capital will be based on security instead of equity, you should also specify the source of collateral.

- Current business position. Furnishes relevant information about the company, its legal form of operation, when it was formed, the principal owners and key personnel.

- Major achievements. Details any developments within the company that are essential to the success of the business. Major achievements include items like patents, prototypes, location of a facility, any crucial contracts that need to be in place for product development, or results from any test marketing that has been conducted.

When writing your statement of purpose, don't waste words. If the statement of purpose is eight pages, nobody's going to read it because it'll be very clear that the business, no matter what its merits, won't be a good investment because the principals are indecisive and don't really know what they want. Make it easy for the reader to realize at first glance both your needs and capabilities.

Business Description

Tell them all about it.

The business description usually begins with a short description of the industry. When describing the industry, discuss the present outlook as well as future possibilities. You should also provide information on all the various markets within the industry, including any new products or developments that will benefit or adversely affect your business. Base all of your observations on reliable data and be sure to footnote sources of information as appropriate. This is important if you're seeking funding; the investor will want to know just how dependable your information is, and won't risk money on assumptions or conjecture.

When describing your business, the first thing you need to concentrate on is its structure. By structure we mean the type of operation, i.e. wholesale, retail, food service, manufacturing or service-oriented. Also state whether the business is new or already established.

In addition to structure, legal form should be reiterated once again. Detail whether the business is a sole proprietorship, partnership or corporation, who its principals are, and what they will bring to the business.

You should also mention who you will sell to, how the product will be distributed, and the business's support systems. Support may come in the form of advertising, promotions and customer service.

Once you've described the business, you need to describe the products or services you intend to market. The product description statement should be complete enough to give the reader a clear idea of your intentions. You may want to emphasize any unique features or variations from concepts that can typically be found in the industry.

Be specific in showing how you will give your business a competitive edge. For example, your business will be better because you will supply a full line of products; competitor A doesn't have a full line. You're going to provide service after the sale; competitor B doesn't support anything he sells. Your merchandise will be of higher quality. You'll give a money-back guarantee. Competitor C has the reputation for selling the best French fries in town; you're going to sell the best Thousand Island dressing.

How Will I Profit?

Now you must be a classic capitalist and ask yourself, "How can I turn a buck? And why do I think I can make a profit that way?" Answer that question for yourself, and then convey that answer to others in the business concept section. You don't have to write 25 pages on why your business will be profitable. Just explain the factors you think will make it successful, like the following: it's a well-organized business, it will have state-of-the-art equipment, its location is exceptional, the market is ready for it, and it's a dynamite product at a fair price.

If you're using your business plan as a document for financial purposes, explain why the added equity or debt money is going to make your business more profitable.

Show how you will expand your business or be able to create something by using that money.

Show why your business is going to be profitable. A potential lender is going to want to know how successful you're going to be in this particular business. Factors that support your claims for success can be mentioned briefly; they will be detailed later. Give the reader an idea of the experience of the other key people in the business. They'll want to know what suppliers or experts you've spoken to about your business and their response to your idea. They may even ask you to clarify your choice of location or reasons for selling this particular product.

The business description can be a few paragraphs in length to a few pages, depending on the complexity of your plan. If your plan isn't too complicated, keep your business description short, describing the industry in one paragraph, the product in another, and the business and its success factors in three or four paragraphs that will end the statement.

While you may need to have a lengthy business description in some cases, it's our opinion that a short statement conveys the required information in a much more effective manner. It doesn't attempt to hold the reader's attention for an extended period of time, and this is important if you're presenting to a potential investor who will have other plans he or she will need to read as well. If the business description is long and drawn-out, you'll lose the reader's attention, and possibly any chance of receiving the necessary funding for the project.

Market Strategies

Define your market.

Market strategies are the result of a meticulous market analysis. A market analysis forces the entrepreneur to become familiar with all aspects of the market so that the target market can be defined and the company can be positioned in order to garner its share of sales. A market analysis also enables the entrepreneur to establish pricing, distribution and promotional strategies that will allow the company to become profitable within a competitive environment. In addition, it provides an indication of the growth potential within the industry, and this will allow you to develop your own estimates for the future of your business.

Begin your market analysis by defining the market in terms of size, structure, growth prospects, trends and sales potential.

The total aggregate sales of your competitors will provide you with a fairly accurate estimate of the total potential market. Once the size of the market has been determined, the next step is to define the target market. The target market narrows down the total market by concentrating on segmentation factors that will determine the total addressable market--the total number of users within the sphere of the business's influence. The segmentation factors can be geographic, customer attributes or product-oriented.

For instance, if the distribution of your product is confined to a specific geographic area, then you want to further define the target market to reflect the number of users or sales of that product within that geographic segment.

Once the target market has been detailed, it needs to be further defined to determine the total feasible market. This can be done in several ways, but most professional planners will delineate the feasible market by concentrating on product segmentation factors that may produce gaps within the market. In the case of a microbrewery that plans to brew a premium lager beer, the total feasible market could be defined by determining how many drinkers of premium pilsner beers there are in the target market.

It's important to understand that the total feasible market is the portion of the market that can be captured provided every condition within the environment is perfect and there is very little competition. In most industries this is simply not the case. There are other factors that will affect the share of the feasible market a business can reasonably obtain. These factors are usually tied to the structure of the industry, the impact of competition, strategies for market penetration and continued growth, and the amount of capital the business is willing to spend in order to increase its market share.

Projecting Market Share

Arriving at a projection of the market share for a business plan is very much a subjective estimate. It's based on not only an analysis of the market but on highly targeted and competitive distribution, pricing and promotional strategies. For instance, even though there may be a sizable number of premium pilsner drinkers to form the total feasible market, you need to be able to reach them through your distribution network at a price point that's competitive, and then you have to let them know it's available and where they can buy it. How effectively you can achieve your distribution, pricing and promotional goals determines the extent to which you will be able to garner market share.

For a business plan, you must be able to estimate market share for the time period the plan will cover. In order to project market share over the time frame of the business plan, you'll need to consider two factors:

- Industry growth which will increase the total number of users. Most projections utilize a minimum of two growth models by defining different industry sales scenarios. The industry sales scenarios should be based on leading indicators of industry sales, which will most likely include industry sales, industry segment sales, demographic data and historical precedence.

- Conversion of users from the total feasible market. This is based on a sales cycle similar to a product life cycle where you have five distinct stages: early pioneer users, early users, early majority users, late majority users and late users. Using conversion rates, market growth will continue to increase your market share during the period from early pioneers to early majority users, level off through late majority users, and decline with late users.

Defining the market is but one step in your analysis. With the information you've gained through market research, you need to develop strategies that will allow you to fulfill your objectives.

Positioning Your Business

When discussing market strategy, it's inevitable that positioning will be brought up. A company's positioning strategy is affected by a number of variables that are closely tied to the motivations and requirements of target customers within as well as the actions of primary competitors.

Before a product can be positioned, you need to answer several strategic questions such as:

- How are your competitors positioning themselves?

- What specific attributes does your product have that your competitors' don't?

- What customer needs does your product fulfill?

Once you've answered your strategic questions based on research of the market, you can then begin to develop your positioning strategy and illustrate that in your business plan. A positioning statement for a business plan doesn't have to be long or elaborate. It should merely point out exactly how you want your product perceived by both customers and the competition.

How you price your product is important because it will have a direct effect on the success of your business. Though pricing strategy and computations can be complex, the basic rules of pricing are straightforward:

- All prices must cover costs.

- The best and most effective way of lowering your sales prices is to lower costs.

- Your prices must reflect the dynamics of cost, demand, changes in the market and response to your competition.

- Prices must be established to assure sales. Don't price against a competitive operation alone. Rather, price to sell.

- Product utility, longevity, maintenance and end use must be judged continually, and target prices adjusted accordingly.

- Prices must be set to preserve order in the marketplace.

There are many methods of establishing prices available to you:

- Cost-plus pricing. Used mainly by manufacturers, cost-plus pricing assures that all costs, both fixed and variable, are covered and the desired profit percentage is attained.

- Demand pricing. Used by companies that sell their product through a variety of sources at differing prices based on demand.

- Competitive pricing. Used by companies that are entering a market where there is already an established price and it is difficult to differentiate one product from another.

- Markup pricing. Used mainly by retailers, markup pricing is calculated by adding your desired profit to the cost of the product. Each method listed above has its strengths and weaknesses.

- Distribution

Distribution includes the entire process of moving the product from the factory to the end user. The type of distribution network you choose will depend upon the industry and the size of the market. A good way to make your decision is to analyze your competitors to determine the channels they are using, then decide whether to use the same type of channel or an alternative that may provide you with a strategic advantage.

Some of the more common distribution channels include:

- Direct sales. The most effective distribution channel is to sell directly to the end-user.

- OEM (original equipment manufacturer) sales. When your product is sold to the OEM, it is incorporated into their finished product and it is distributed to the end user.

- Manufacturer's representatives. One of the best ways to distribute a product, manufacturer's reps, as they are known, are salespeople who operate out of agencies that handle an assortment of complementary products and divide their selling time among them.

- Wholesale distributors. Using this channel, a manufacturer sells to a wholesaler, who in turn sells it to a retailer or other agent for further distribution through the channel until it reaches the end user.

- Brokers. Third-party distributors who often buy directly from the distributor or wholesaler and sell to retailers or end users.

- Retail distributors. Distributing a product through this channel is important if the end user of your product is the general consuming public.

- Direct Mail. Selling to the end user using a direct mail campaign.

As we've mentioned already, the distribution strategy you choose for your product will be based on several factors that include the channels being used by your competition, your pricing strategy and your own internal resources.

Promotion Plan

With a distribution strategy formed, you must develop a promotion plan. The promotion strategy in its most basic form is the controlled distribution of communication designed to sell your product or service. In order to accomplish this, the promotion strategy encompasses every marketing tool utilized in the communication effort. This includes:

- Advertising. Includes the advertising budget, creative message(s), and at least the first quarter's media schedule.

- Packaging. Provides a description of the packaging strategy. If available, mockups of any labels, trademarks or service marks should be included.

- Public relations. A complete account of the publicity strategy including a list of media that will be approached as well as a schedule of planned events.

- Sales promotions. Establishes the strategies used to support the sales message. This includes a description of collateral marketing material as well as a schedule of planned promotional activities such as special sales, coupons, contests and premium awards.

- Personal sales. An outline of the sales strategy including pricing procedures, returns and adjustment rules, sales presentation methods, lead generation, customer service policies, salesperson compensation, and salesperson market responsibilities.

Sales Potential

Once the market has been researched and analyzed, conclusions need to be developed that will supply a quantitative outlook concerning the potential of the business. The first financial projection within the business plan must be formed utilizing the information drawn from defining the market, positioning the product, pricing, distribution, and strategies for sales. The sales or revenue model charts the potential for the product, as well as the business, over a set period of time. Most business plans will project revenue for up to three years, although five-year projections are becoming increasingly popular among lenders.

When developing the revenue model for the business plan, the equation used to project sales is fairly simple. It consists of the total number of customers and the average revenue from each customer. In the equation, "T" represents the total number of people, "A" represents the average revenue per customer, and "S" represents the sales projection. The equation for projecting sales is: (T)(A) = S

Using this equation, the annual sales for each year projected within the business plan can be developed. Of course, there are other factors that you'll need to evaluate from the revenue model. Since the revenue model is a table illustrating the source for all income, every segment of the target market that is treated differently must be accounted for. In order to determine any differences, the various strategies utilized in order to sell the product have to be considered. As we've already mentioned, those strategies include distribution, pricing and promotion.

Competitive Analysis

Identify and analyze your competition.

The competitive analysis is a statement of the business strategy and how it relates to the competition. The purpose of the competitive analysis is to determine the strengths and weaknesses of the competitors within your market, strategies that will provide you with a distinct advantage, the barriers that can be developed in order to prevent competition from entering your market, and any weaknesses that can be exploited within the product development cycle.

The first step in a competitor analysis is to identify the current and potential competition. There are essentially two ways you can identify competitors. The first is to look at the market from the customer's viewpoint and group all your competitors by the degree to which they contend for the buyer's dollar. The second method is to group competitors according to their various competitive strategies so you understand what motivates them.

Once you've grouped your competitors, you can start to analyze their strategies and identify the areas where they're most vulnerable. This can be done through an examination of your competitors' weaknesses and strengths. A competitor's strengths and weaknesses are usually based on the presence and absence of key assets and skills needed to compete in the market.

To determine just what constitutes a key asset or skill within an industry, David A. Aaker in his book, Developing Business Strategies , suggests concentrating your efforts in four areas:

- The reasons behind successful as well as unsuccessful firms

- Prime customer motivators

- Major component costs

- Industry mobility barriers

According to theory, the performance of a company within a market is directly related to the possession of key assets and skills. Therefore, an analysis of strong performers should reveal the causes behind such a successful track record. This analysis, in conjunction with an examination of unsuccessful companies and the reasons behind their failure, should provide a good idea of just what key assets and skills are needed to be successful within a given industry and market segment.

Through your competitor analysis, you will also have to create a marketing strategy that will generate an asset or skill competitors don't have, which will provide you with a distinct and enduring competitive advantage. Since competitive advantages are developed from key assets and skills, you should sit down and put together a competitive strength grid. This is a scale that lists all your major competitors or strategic groups based upon their applicable assets and skills and how your own company fits on this scale.

Create a Competitive Strength Grid

To put together a competitive strength grid, list all the key assets and skills down the left margin of a piece of paper. Along the top, write down two column headers: "weakness" and "strength." In each asset or skill category, place all the competitors that have weaknesses in that particular category under the weakness column, and all those that have strengths in that specific category in the strength column. After you've finished, you'll be able to determine just where you stand in relation to the other firms competing in your industry.

Once you've established the key assets and skills necessary to succeed in this business and have defined your distinct competitive advantage, you need to communicate them in a strategic form that will attract market share as well as defend it. Competitive strategies usually fall into these five areas:

- Advertising

Many of the factors leading to the formation of a strategy should already have been highlighted in previous sections, specifically in marketing strategies. Strategies primarily revolve around establishing the point of entry in the product life cycle and an endurable competitive advantage. As we've already discussed, this involves defining the elements that will set your product or service apart from your competitors or strategic groups. You need to establish this competitive advantage clearly so the reader understands not only how you will accomplish your goals, but also why your strategy will work.

Design and Development Plan

What you'll cover in this section.

The purpose of the design and development plan section is to provide investors with a description of the product's design, chart its development within the context of production, marketing and the company itself, and create a development budget that will enable the company to reach its goals.

There are generally three areas you'll cover in the development plan section:

- Product development

- Market development

- Organizational development

Each of these elements needs to be examined from the funding of the plan to the point where the business begins to experience a continuous income. Although these elements will differ in nature concerning their content, each will be based on structure and goals.

The first step in the development process is setting goals for the overall development plan. From your analysis of the market and competition, most of the product, market and organizational development goals will be readily apparent. Each goal you define should have certain characteristics. Your goals should be quantifiable in order to set up time lines, directed so they relate to the success of the business, consequential so they have impact upon the company, and feasible so that they aren't beyond the bounds of actual completion.

Goals For Product Development

Goals for product development should center on the technical as well as the marketing aspects of the product so that you have a focused outline from which the development team can work. For example, a goal for product development of a microbrewed beer might be "Produce recipe for premium lager beer" or "Create packaging for premium lager beer." In terms of market development, a goal might be, "Develop collateral marketing material." Organizational goals would center on the acquisition of expertise in order to attain your product and market-development goals. This expertise usually needs to be present in areas of key assets that provide a competitive advantage. Without the necessary expertise, the chances of bringing a product successfully to market diminish.

With your goals set and expertise in place, you need to form a set of procedural tasks or work assignments for each area of the development plan. Procedures will have to be developed for product development, market development, and organization development. In some cases, product and organization can be combined if the list of procedures is short enough.

Procedures should include how resources will be allocated, who is in charge of accomplishing each goal, and how everything will interact. For example, to produce a recipe for a premium lager beer, you would need to do the following:

- Gather ingredients.

- Determine optimum malting process.

- Gauge mashing temperature.

- Boil wort and evaluate which hops provide the best flavor.

- Determine yeast amounts and fermentation period.

- Determine aging period.

- Carbonate the beer.

- Decide whether or not to pasteurize the beer.

The development of procedures provides a list of work assignments that need to be accomplished, but one thing it doesn't provide are the stages of development that coordinate the work assignments within the overall development plan. To do this, you first need to amend the work assignments created in the procedures section so that all the individual work elements are accounted for in the development plan. The next stage involves setting deliverable dates for components as well as the finished product for testing purposes. There are primarily three steps you need to go through before the product is ready for final delivery:

- Preliminary product review . All the product's features and specifications are checked.

- Critical product review . All the key elements of the product are checked and gauged against the development schedule to make sure everything is going according to plan.

- Final product review . All elements of the product are checked against goals to assure the integrity of the prototype.

Scheduling and Costs

This is one of the most important elements in the development plan. Scheduling includes all of the key work elements as well as the stages the product must pass through before customer delivery. It should also be tied to the development budget so that expenses can be tracked. But its main purpose is to establish time frames for completion of all work assignments and juxtapose them within the stages through which the product must pass. When producing the schedule, provide a column for each procedural task, how long it takes, start date and stop date. If you want to provide a number for each task, include a column in the schedule for the task number.

Development Budget